What You Need to Know About Land-Use Change Accounting: The New GHG Protocol Land Sector and Removals Standard

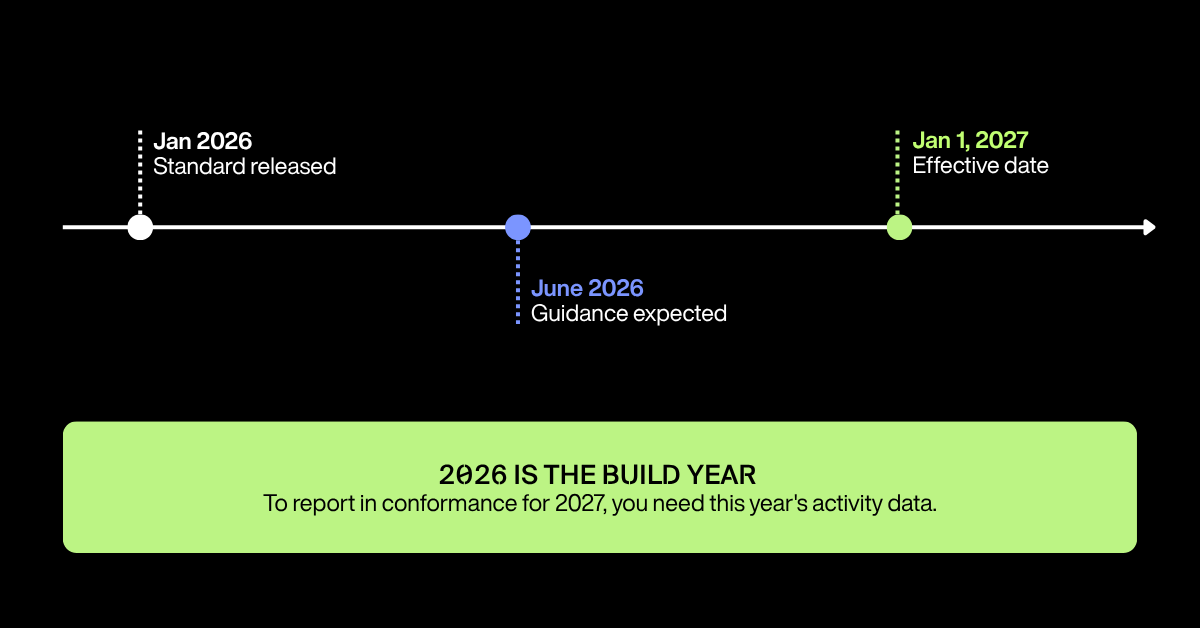

For most companies, land emissions have been the roughest part of the carbon inventory, estimated loosely or left out. The GHG Protocol's Land Sector and Removals Standard, released in January 2026, changes that. If you source agricultural commodities, fiber, or other land-intensive materials, it sets new requirements for how you account for those emissions, and the first compliant inventory will be built on 2026 data. So the work starts this year, not when the Standard takes effect in 2027.

What is the Land Sector and Removals Standard?

The Land Sector and Removals Standard (LSR Standard, sometimes written LSRS) is the first global corporate accounting framework for land emissions and carbon removals. The GHG Protocol released it on January 30, 2026, after a five-year, multi-stakeholder process. It standardizes how companies account for land-use change, land management emissions, agricultural emissions, and CO₂ removals, areas where, until now, companies relied on inconsistent and largely incomparable methods.

It's a supplement to the GHG Protocol's existing Corporate Standard and Scope 3 Standard, not a replacement. You still build your inventory the way you always have. The LSR Standard adds land sector-specific requirements on top.

Standard vs. Guidance: what's the difference, and what's publishing in June 2026?

This trips people up, because the names are nearly identical. There are two documents:

• The Standard (released January 2026) sets the requirements. It's the conformance document, what you must do, written as "shall" statements. It contains 32 requirements across the full land sector.

• The Guidance (expected Q2 2026) is the implementation companion. It adds equations, worked examples, and case studies from pilot-testing companies to help you apply the requirements. It does not change what's required.

Our recommendation: don't wait for the Guidance to start. The requirements are already final, and the Guidance will help you implement them, not change them. (Worth noting: forest carbon accounting isn't in this version of the Standard. The GHG Protocol deferred it to a future iteration, so the current rules cover land-use change from sourcing, agricultural land management, and removals, but not standalone forest carbon.)

Does the GHG Protocol now require land-use change accounting?

Yes, for companies with significant land sector activities. If you own or control land, or you purchase or sell products produced on agricultural land, or you have other land-based activities in your value chain, land-use change is now something you account for systematically rather than estimate loosely or skip.

The first question to answer is whether you have "significant" land sector activities in your operations or supply chain. If you buy meaningful volumes of agricultural commodities, that answer is usually yes.

When does it take effect, and why does that mean acting now?

The Standard takes effect January 1, 2027. That sounds far off until you do the math on the reporting cycle.

To report in conformance for 2027, you need 2026 activity data; that's this year's data. The first compliant inventory will be built on numbers you're either collecting now or wishing you had. For companies with material exposure, "we'll deal with it next year" doesn't work, because supplier engagement, traceability systems, and data governance take time to stand up, and they have to be running on this year's data.

Which sectors are in scope?

This is much broader than agriculture companies. Any sector with land-intensive supply chains can fall in scope:

• Food and beverage, where ingredients carry the land footprint of where they were grown.

• Apparel and textiles, through cotton, leather, and other land-based fibers.

• Paper, paper products, and packaging, through wood pulp and fiber sourcing. Take bamboo toilet paper as an example: the marketing leans on "better for the planet," but the land question is where and how the bamboo is grown, and whether that land was recently converted. The land-use story sits underneath the product claim, and now it has to be measured.

• Consumer goods, bioenergy, and mining, each with their own land exposure.

The material contribution here is real. Emissions from agriculture and land-use change account for roughly a quarter of global greenhouse gas emissions. For a consumer brand, the land footprint of sourced commodities is often a large and previously under-counted share of the Scope 3 inventory.

What changes in how I build my inventory?

The biggest structural change: land-sector emissions and removals can no longer be folded into a single Scope 1–3 total without additional disclosure. Three specific shifts follow.

You separate land-sector impacts from the rest of the inventory. You identify emissions from land-sector activities (agriculture, land-use change, soil management) and distinguish them from non-land-sector emissions.

You report removals separately from emissions. You can't use removals to net down your gross emissions into a single figure. Gross emissions and removals are disclosed separately.

Your inventory gets more disaggregated. Expect additional reporting tables and disclosures, not just one CO₂e figure. Your corporate inventory documentation will need to spell out land-sector boundaries, classifications, estimation methods, assumptions, and how you treated removals and storage.

The practical translation: more granular data, more documentation, and a higher bar for data quality than most companies are used to clearing on the land side.

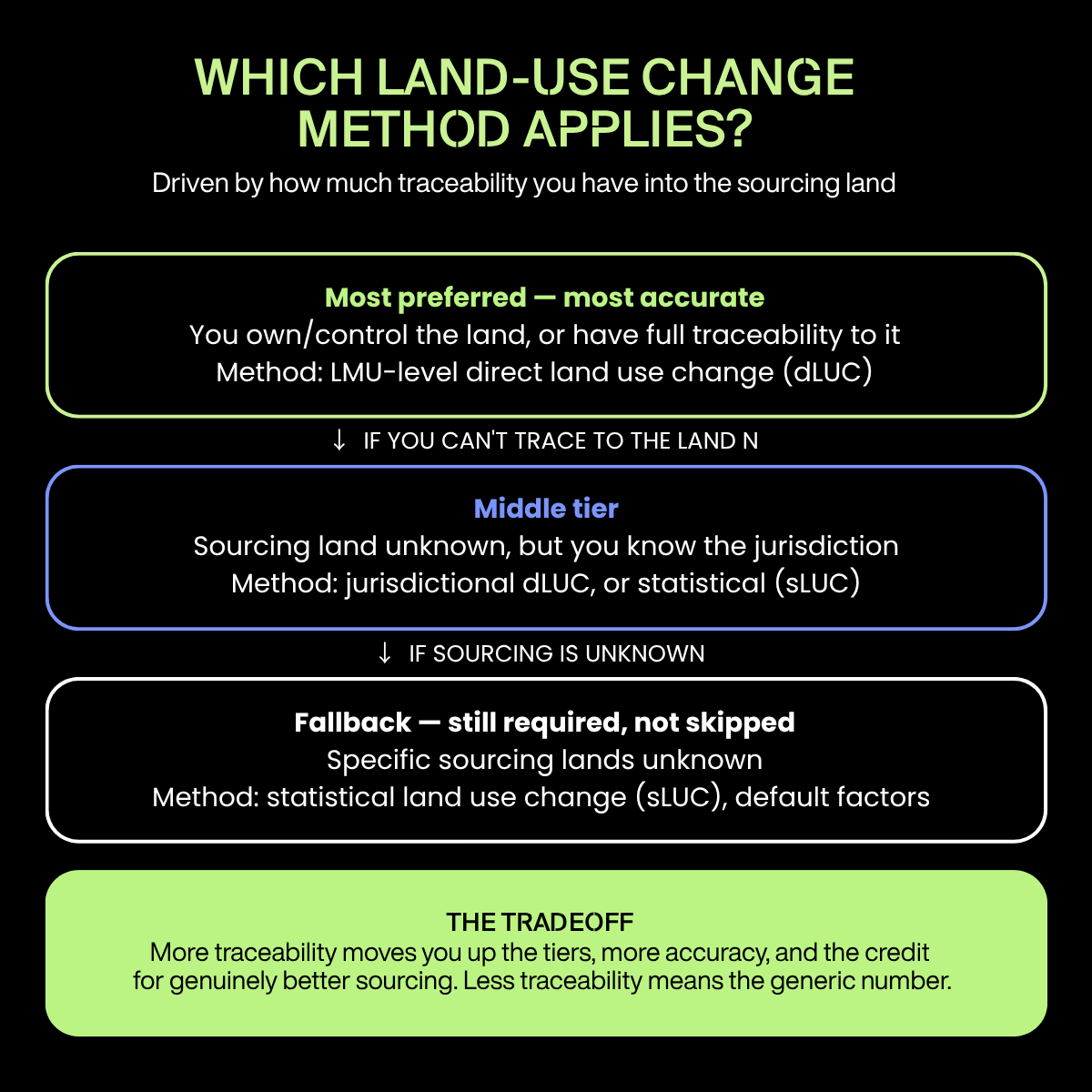

How do I account for land-use change emissions? What’s the methodological hierarchy?

This is where the Standard gets specific, and where our scientific take matters most. The Standard sets a preference order for how you calculate land-use change emissions, driven by how much traceability you have into your supply chain.

First preference: direct land-use change (dLUC) at the land-management-unit level. If you own or control the land, or you have complete traceability to the specific lands in your value chain, you use the actual location, timing, and extent of land conversion. This is the most accurate and the most data-hungry.

Second preference: jurisdictional dLUC. When you don't know the specific sourcing lands but you know the jurisdiction, you use regional or jurisdiction-specific activity data and emission factors that reflect local land-use dynamics.

Lowest tier: statistical land-use change (sLUC). When specific sourcing lands are unknown, you fall back to statistical emission factors, secondary or default factors that estimate land-use change based on the commodity and broad region. You can use sLUC factors from third-party databases, but you have to verify they apply the correct allocation method and meet the Standard's requirements.

Our position at Planet FWD: if we're building an inventory, we use statistical land-use change, and we include it rather than leaving it out. Statistical methods can capture both direct and market-mediated effects, and "we couldn't trace it perfectly" is not a reason to report zero. The Standard agrees, the fallback isn't "skip it," it's "use the statistical approach." (You can see how we approach this on our methodology page.)

Should indirect land-use change be included?

Yes, and this is a point we feel strongly about. Direct land-use change is the observable, traceable conversion: you cleared this forest to grow this crop. Indirect land-use change is the market-driven displacement: demand for a commodity pushes land conversion somewhere else, with no direct physical link to your specific purchase.

Indirect LUC is an increasingly active debate, much of it stemming from biofuels and the question of what happens to land when cropland grows fuel instead of food. The Standard addresses the indirect piece through a carbon opportunity cost metric for land use, a way to account for the emissions implications of occupying land that could otherwise store carbon. Our view is that leaving indirect effects out understates the real impact, and statistical approaches are well suited to capturing them.

What about traceability and removals specifically?

Carbon removals face the strictest rules in the Standard. If you want to report removals, soil carbon, for instance, you face requirements around traceability, monitoring, permanence, reversals, uncertainty, and double counting. You can't simply claim a removal; you need robust evidence and ongoing tracking. Removals generally require physical traceability to the sourcing region or farm, and "book and claim" certificates are not currently accepted for removal claims.

This is why traceability becomes a central compliance issue rather than a nice-to-have. The precision of everything you report, emissions and removals alike, depends on the quality of your spatial boundaries and traceability data. Knowing where your products originate is what the rest of the inventory rests on.

Are companies doing the right thing getting credit for it?

This is the open question I'm watching most closely.

Picture a company buying palm oil that's certified deforestation-free. Under the Standard, they cannot automatically assign zero land-use-change emissions solely because the product is certified. The standard considers certification as supporting evidence whose usefulness depends on factors such as traceability, chain of custody, assurance, and the certification's temporal scope.

If the company cannot trace its supply to the level required by the chosen accounting approach, it may need to rely on broader regional, jurisdictional, or statistical emission factors rather than supplier-specific land-use-change data. And these generic numbers reflect an area's average deforestation, not necessarily the performance of a potentially much lower impact supply that they bought. The certification alone doesn't lower the calculated number.

A company sourcing better can end up reporting the same land-use-change number because the statistical method works off location, not their specific sourcing decisions. The protocol’s emphasis is on traceability and location-specific evidence, which can be challenging or even prohibitive for many companies to achieve, and certification is increasingly viewed only as supporting evidence, not a standalone reason to assign zero land-use-change emissions.

The open question for our industry is how we make sure the companies doing the right thing get quantitative credit for it. That requires traceability infrastructure that most supply chains don't have yet. It's the data gap I'm watching most closely, because solving it is what turns "better sourcing" from a marketing claim into a measured, defensible reduction.

What should you do now?

If you have material land-sector exposure, the prep work starts with this year's data:

• Assess whether you're in scope. Determine if your land sector activities are "significant" in operations or value chain.

• Start collecting higher-resolution supply chain data. The more traceability you have, the better your numbers and the more credit you can claim for genuinely better sourcing. If you want to report removals, higher-resolution data isn't optional.

• Update your inventory methodology to document land-sector boundaries, classifications, estimation methods, and your treatment of removals.

• Revisit targets and claims to make sure they hold up under the new guidance.

Companies that treat 2026 as the build year will have credible numbers ready for the first reporting cycle. The ones who wait for the 2027 effective date will be reconstructing this year's data after the fact.

___________________________

Planet FWD supports statistical land-use change accounting, including indirect effects, as part of building a defensible land sector inventory. If you're working out what the LSR Standard means for your supply chain, talk to our team.

This is the first of a two-part series. The companion piece, Land-Use Change: Which Commodities Carry the Most Risk, and How to Reduce Your Emissions, covers why land-use change matters beyond compliance, which commodities and locations carry the most risk, and what you can do to reduce land-use-change emissions.

Head of marketing

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Consectetur, adipiscing elit, sed do eiusmod tempor incididunt ut lab. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Lorem ipsum dolor sit amet, consectetur adipiscing elit.

This is an example blog post style

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Sed vulputate odio ut enim. Volutpat sed cras ornare arcu dui. Lorem dolor sed viverra ipsum. Luctus accumsan tortor posuere ac ut consequat semper. Viverra justo nec ultrices dui sapien eget mi proin. Mollis nunc sed id semper risus in hendrerit gravida rutrum. Lacinia quis vel eros donec. Nisi vitae suscipit tellus mauris a diam. Ac orci phasellus egestas tellus rutrum tellus pellentesque eu tincidunt. Morbi quis commodo odio aenean sed adipiscing diam. Urna duis convallis convallis tellus id interdum. Tortor vitae purus faucibus ornare suspendisse sed. Vehicula ipsum a arcu cursus vitae congue. Enim sed faucibus turpis in. Orci eu lobortis elementum nibh tellus molestie nunc non blandit.

Nunc id cursus metus aliquam eleifend mi in. A erat nam at lectus urna duis convallis convallis. Tristique senectus et netus et malesuada fames ac. Id interdum velit laoreet id donec. Egestas dui id ornare arcu odio. Gravida rutrum quisque non tellus orci ac auctor. Malesuada fames ac turpis egestas maecenas pharetra convallis. Ut diam quam nulla porttitor. Eget nunc lobortis mattis aliquam faucibus purus. Aenean sed adipiscing diam donec adipiscing tristique risus nec. Nisi est sit amet facilisis magna etiam tempor orci eu. Tortor posuere ac ut consequat.

“Lorem ipsum dolor sit amet, consectetur adipiscing elit”

<span class="blockquote-wrap">

<strong>Naomi</strong>

Head of marketing

</span>

This is an example blog post style

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Sed vulputate odio ut enim. Volutpat sed cras ornare arcu dui. Lorem dolor sed viverra ipsum. Luctus accumsan tortor posuere ac ut consequat semper. Viverra justo nec ultrices dui sapien eget mi proin. Mollis nunc sed id semper risus in hendrerit gravida rutrum. Lacinia quis vel eros donec. Nisi vitae suscipit tellus mauris a diam. Ac orci phasellus egestas tellus rutrum tellus pellentesque eu tincidunt. Morbi quis commodo odio aenean sed adipiscing diam. Urna duis convallis convallis tellus id interdum. Tortor vitae purus faucibus ornare suspendisse sed. Vehicula ipsum a arcu cursus vitae congue. Enim sed faucibus turpis in. Orci eu lobortis elementum nibh tellus molestie nunc non blandit.

<span class="rtb-protip">

<span class="rtb-protip-title"></span>

<span class="rtb-protip-body">Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim.</span></span>

How to customize formatting for each rich text

- Lorem ipsum dolor sit amet, consectetur adipiscing elit sed do eiusmod

- Lorem ipsum dolor sit amet, consectetur adipiscing elit sed do eiusmod

- Lorem ipsum dolor sit amet, consectetur adipiscing elit sed do eiusmod

- Lorem ipsum dolor sit amet, consectetur adipiscing elit sed do eiusmod

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.

Static and dynamic content editing

A rich text element can be used with static or dynamic content. For static content, just drop it into any page and begin editing. For dynamic content, add a rich text field to any collection and then connect a rich text element to that field in the settings panel. Voila!

- Lorem ipsum dolor sit amet, consectetur adipiscing elit sed do eiusmod

- For static content, just drop it into any page and begin editing. For static content, just drop it into any page and begin editing.

- Lorem ipsum dolor sit amet, consectetur adipiscing

How to customize formatting for each heading

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.